On October 1, 2023, Ian Ackerley stepped down from his role, with his tenure marked by challenges in managing customer expectations and service delivery. His successor, who has yet to be named, will need to address the backlog of transactions that has affected many savers, particularly those relying on NS&I products for their financial security. For further insights into similar leadership dynamics, refer to Powell Will Stay as Fed Chair Until Successor Is Confirmed.

This leadership transition is critical as NS&I plays a vital role in the UK’s savings landscape, offering various products including Premium Bonds and fixed-rate accounts. The delays have raised questions about the operational efficiency of the organization and its ability to serve the public effectively.

With the UK economy facing various pressures, including rising inflation and interest rates, the timely management of savings is more crucial than ever. Stakeholders are calling for immediate action to resolve the issues at hand, emphasizing the need for transparency and improved communication from the new leadership.

Understanding the background of NS&I and its operations

The National Savings and Investments (NS&I) has a long-standing history as a government-backed savings organization in the United Kingdom, established in 1861. Initially designed to help fund government borrowing during times of war, NS&I has evolved into a key player in the UK savings market, offering a range of savings products, including Premium Bonds, savings accounts, and investment products. Its unique position as a state-owned entity allows it to provide secure savings options for the public while also contributing to the government’s financing needs. Understanding the broader implications of governmental roles can add context; for example, see how Trump’s war in Iran reveals a shift in US foreign policy.

Over the years, NS&I has faced various challenges, particularly in adapting to changing economic conditions and consumer expectations. The low-interest-rate environment that has persisted since the financial crisis of 2008 has significantly impacted the attractiveness of NS&I’s offerings. Savers have increasingly sought higher returns elsewhere, leading to a decline in NS&I’s customer base and prompting the organization to rethink its strategy and product offerings.

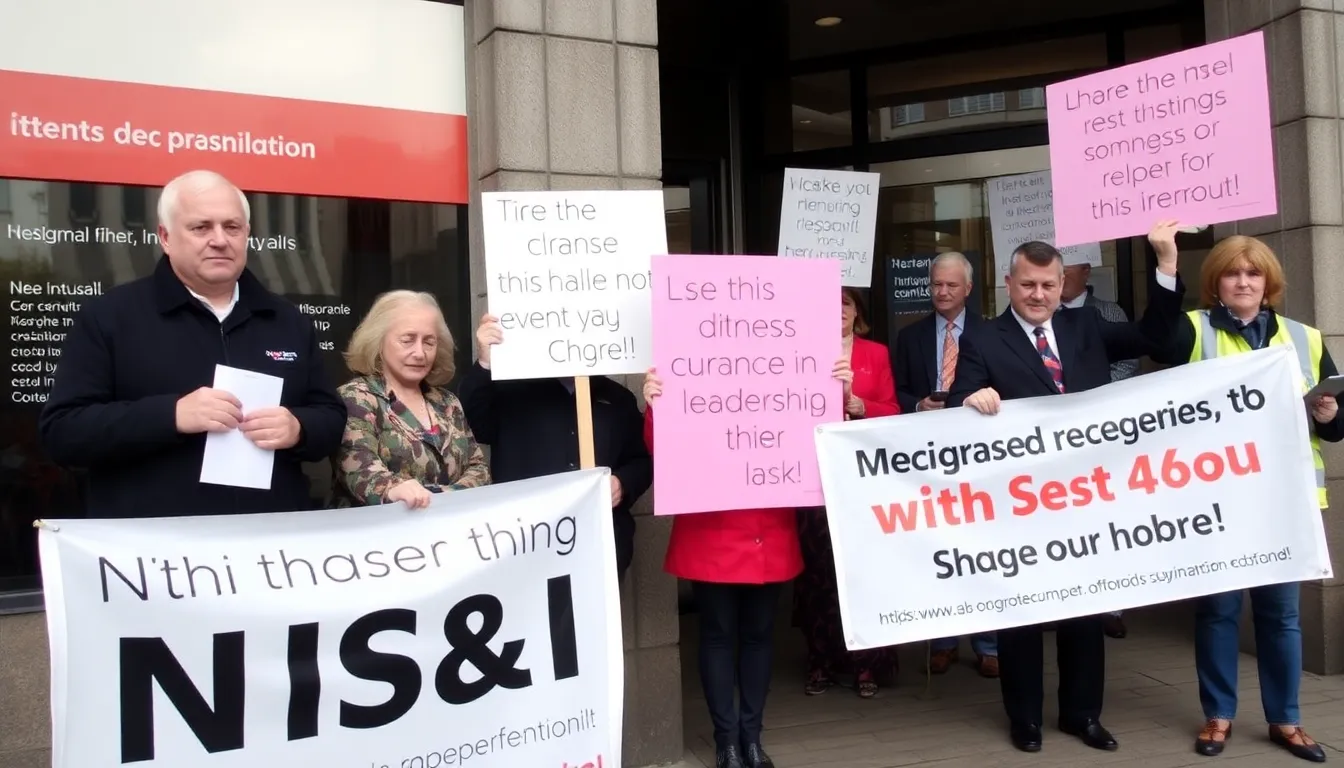

In recent months, the issue of delayed payments and customer service failures has come to the forefront, leaving many savers frustrated and uncertain about their investments. As NS&I has grappled with an influx of inquiries and claims, the operational inefficiencies have led to significant public dissatisfaction. This situation has been exacerbated by the broader economic climate, where rising inflation has heightened the urgency for savers to access their funds.

Key Milestones and Recent Developments

The leadership changes within NS&I reflect a response to these mounting pressures. The recent replacement of the NS&I boss was a pivotal moment aimed at restoring public confidence and improving operational efficiency. This transition comes amid growing scrutiny from regulators and the government, as NS&I seeks to address systemic issues that have left millions of pounds unclaimed and savers waiting for resolutions.

As NS&I moves forward, it faces the challenge of not only regaining the trust of its customers but also adapting to an increasingly competitive savings landscape. The organization must navigate these complexities while ensuring it meets its dual mandate of supporting savers and contributing to national financial stability.

Key stakeholders and issues surrounding the leadership change

The recent replacement of the National Savings and Investments (NS&I) boss has raised significant concerns among various stakeholders, primarily savers, government officials, and financial analysts. Each group has distinct interests that influence their perspectives on the leadership change and its implications for the organization and its customers.

Savers, who have been left waiting for millions of pounds in payouts, are understandably anxious about the transition in leadership. Their primary interest lies in ensuring that their savings are secure and that the organization remains efficient in processing withdrawals and payouts. Delays in these transactions can lead to a loss of trust and confidence in NS&I, which is particularly troubling for those relying on these savings for essential needs.

On the governmental side, NS&I operates under the aegis of the Treasury, which has an interest in maintaining public confidence in government-backed savings products. The leadership change may prompt scrutiny over the organization’s operational efficiency and its ability to deliver on its promises to savers. Additionally, the government has a vested interest in ensuring that NS&I continues to fulfill its mandate to support national savings while also contributing to public finances. For insights on how other sectors are adapting, check As wages soar will EFL lose appeal for foreign investors.

Financial analysts and industry experts are also key stakeholders in this situation. They are likely to focus on the implications of the leadership change for NS&I’s strategic direction and overall performance in the competitive savings market. Analysts may assess how the new leadership will address existing challenges, such as low interest rates and the need for innovative savings products that appeal to a broader audience.

- Delay in payouts: Savers are facing uncertainty regarding when they will receive their funds, raising concerns about liquidity.

- Government oversight: The Treasury may increase scrutiny on NS&I’s operations to ensure accountability during the transition.

- Market competitiveness: The leadership change could influence NS&I’s ability to compete with other financial institutions offering attractive savings products.

- Public trust: Maintaining public confidence in NS&I’s reliability is crucial, especially during periods of leadership transition.

- Strategic direction: The new leadership’s vision will be critical in addressing existing challenges and shaping the future of NS&I.

How the leadership transition affects savers and the market

The recent replacement of the NS&I boss has sent ripples through the savings market, affecting various groups including individual savers, financial institutions, and policymakers. Savers who rely on NS&I for secure investments are particularly impacted, as they face uncertainty regarding the future direction of the organization and the products it offers. Additionally, financial institutions that compete with NS&I may also feel the pressure to adjust their offerings in response to any changes in NS&I’s strategy.

In the short term, savers may experience delays in accessing their funds or receiving updates about their investments, leading to frustration and anxiety. This situation could prompt some individuals to reconsider their savings strategies, potentially shifting their funds to other financial institutions. For businesses that rely on stable savings products to manage their cash flow, the uncertainty may disrupt financial planning and investment decisions.

Mid-term impacts could include a reevaluation of savings rates across the industry. As NS&I adjusts its policies under new leadership, other banks and financial institutions may respond by altering their interest rates, either to remain competitive or to attract customers who are dissatisfied with NS&I. This could lead to both risks and opportunities in the savings landscape.

- Risks: Potential loss of customer trust in NS&I, leading to a decline in new investments.

- Opportunities: Competitors may capitalize on the situation by offering more attractive rates or innovative savings products.

- Policy Impacts: Regulatory bodies may reassess oversight of NS&I, which could lead to changes in how savings products are structured.

Overall, the leadership transition at NS&I not only impacts individual savers but also has broader implications for the financial market and policy landscape. Stakeholders across the board will need to navigate this period of uncertainty carefully, balancing risks with the potential for new opportunities in the savings sector.

A: The NS&I boss was replaced amid growing concerns about delays in processing savers’ funds, which have left many customers frustrated. A: The leadership change may initially cause further delays, but it is hoped that new management will streamline operations and improve service. A: NS&I provides a range of savings and investment products, backed by the government, making it a key player in the UK savings landscape. A: Currently, there are no immediate changes to NS&I products, but customers should stay informed about any future updates. A: Customers can contact NS&I through their official website or customer service hotline for any inquiries regarding their accounts.

Frequently asked questions about NS&I changes

Looking ahead: implications for NS&I and its customers

The recent leadership change at NS&I comes at a critical time as the organization grapples with the expectations of millions of savers awaiting their funds. This transition may signal a shift in strategy that could impact customer service and product offerings. As NS&I seeks to reassure its customer base, it will be essential to monitor how these changes affect both operational efficiency and the overall trust in the institution.

Customers should remain vigilant regarding updates on their savings and any changes in interest rates or product availability. The new leadership may bring fresh perspectives on addressing the backlog of payments and improving customer communication, which has been a point of concern. Observing how NS&I adapts to these challenges will be crucial for savers looking to maximize their returns and ensure their investments are secure.

- Leadership Transition: Watch for new strategies that may emerge under the new boss, particularly in customer engagement and service efficiency.

- Payment Backlog Resolution: Keep an eye on how quickly NS&I addresses the pending payments to savers, which will be a key indicator of their operational effectiveness.

- Interest Rate Adjustments: Monitor any changes in interest rates that could impact savings products and overall customer satisfaction.

- Customer Communication: Evaluate improvements in transparency and communication from NS&I, which will be vital for restoring trust among savers.

- Future Product Offerings: Look for potential innovations or changes in NS&I’s product lineup that may better meet the needs of savers in a competitive market.