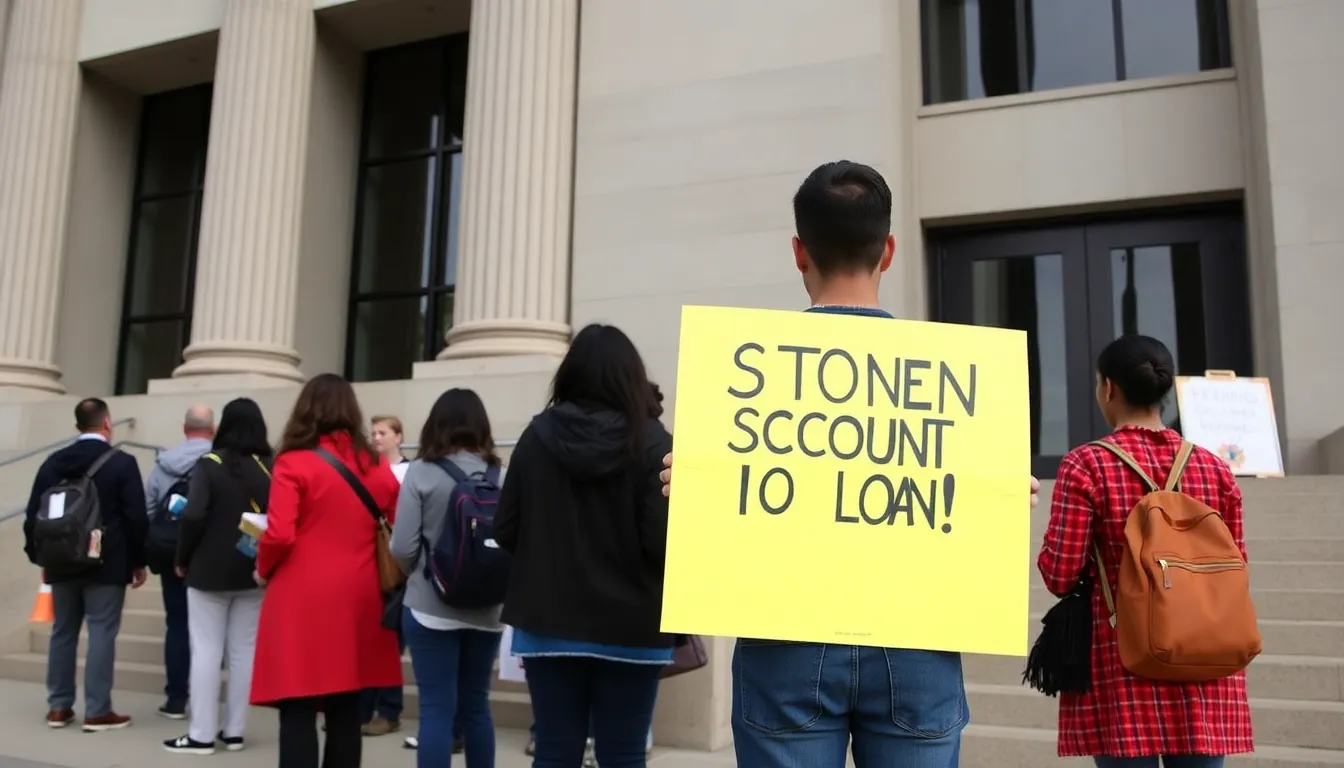

According to data from the American Bankruptcy Institute, approximately 2,000 student loan borrowers filed for bankruptcy in the first half of 2023, a marked increase from previous years. The legal landscape surrounding student loans has evolved, with some judges more willing to grant discharges based on the undue hardship standard. This shift is critical as many borrowers struggle with the financial burden of student debt, often leading to long-term economic hardship.

The rise in successful discharges also reflects broader conversations about the student loan crisis in the United States. Advocates argue that the current system disproportionately affects low-income and marginalized communities, trapping them in cycles of debt. As more borrowers navigate the bankruptcy process, there is a growing call for reforms to make student loans more manageable and to ensure equitable access to education.

This evolving situation is crucial to monitor, as it could influence future policies and the overall discourse surrounding student loans in America.

Understanding the evolving landscape of student loan bankruptcy

The issue of student loan debt and its dischargeability in bankruptcy has undergone significant changes over the past few decades. Historically, student loans were treated similarly to other forms of debt, allowing borrowers to seek relief through bankruptcy. However, the landscape shifted dramatically in the 1970s and 1980s when lawmakers began to impose stricter regulations on the dischargeability of student loans, largely due to concerns about rising default rates and the financial stability of federal loan programs.

This legal standard has proven to be a significant hurdle for many borrowers, as courts have interpreted it narrowly, similar to the challenges discussed in recent legislative changes.

Recent Trends and Legislative Changes

Notable cases, such as the 2020 ruling in the case of Brunner v. New York State Higher Education Services Corporation, have set precedents that may influence future decisions, which is in line with ongoing discussions about bankruptcy reforms.

Additionally, advocacy groups and lawmakers are pushing for reforms to make it easier for borrowers to discharge student loans in bankruptcy. Proposals include legislative changes to the Bankruptcy Code and increased awareness of the challenges faced by borrowers. As public sentiment shifts towards recognizing the burden of student debt, the potential for significant changes in how student loans are treated in bankruptcy proceedings appears to be on the horizon.

Key stakeholders and their perspectives on student loan bankruptcy

As the conversation surrounding student loan bankruptcy evolves, various stakeholders emerge with distinct interests and concerns. These include borrowers, lenders, educational institutions, policymakers, and advocacy groups. Each group presents a unique viewpoint on the implications of allowing student loan debts to be discharged in bankruptcy.

Borrowers, particularly those facing financial hardship, often view bankruptcy as a potential lifeline. Many individuals believe that the ability to discharge student loans would provide them with a fresh start, allowing them to rebuild their financial lives without the burden of insurmountable debt. However, this perspective is complicated by the fear of the long-term impact on credit scores and the potential stigma associated with bankruptcy.

Lenders and financial institutions, on the other hand, have a vested interest in maintaining the current protections against discharging student loans in bankruptcy. They argue that allowing such discharges could lead to increased risk in lending, potentially driving up interest rates for future borrowers. This concern is compounded by the significant amount of federal and private capital tied to student loans, which could be jeopardized if bankruptcy becomes a more accessible option.

Educational institutions also play a critical role in this debate. Many colleges and universities depend on tuition revenue from student loans to fund their operations. If borrowers are able to shed their debts through bankruptcy, institutions may face financial instability, which could lead to increased tuition rates or reduced services for students. This creates a tension between the need to support students and the financial viability of educational institutions.

- Borrowers: Seeking relief from unmanageable debt.

- Lenders: Concerned about financial stability and risk management.

- Educational Institutions: Focused on maintaining revenue streams and institutional integrity.

- Policymakers: Tasked with balancing the interests of all stakeholders while addressing the broader economic implications.

- Advocacy Groups: Aiming to support borrower rights and promote equitable access to education.

The effects of bankruptcy on borrowers and the economy

The recent trend of student loan borrowers successfully discharging their debts through bankruptcy is reshaping the financial landscape for various groups. Primarily, recent graduates and individuals burdened by significant student debt are directly affected. These borrowers often come from diverse socioeconomic backgrounds, including low-income families and first-generation college students, who face the most significant challenges in repaying their loans.

Industries such as education and financial services are also impacted. Educational institutions may see a decline in enrollment as potential students weigh the risks of accumulating debt against the possibility of future bankruptcy. Financial institutions, particularly those offering student loans, might face increased scrutiny and regulatory changes as policymakers respond to the rising number of bankruptcies.

In the short term, the ability to discharge student loans in bankruptcy can relieve financial pressure on borrowers, allowing them to redirect their resources toward essential expenses such as housing and healthcare. This newfound financial freedom can stimulate local economies as individuals have more disposable income to spend. However, there are risks involved; lenders may tighten credit access, making it more difficult for future students to secure loans.

- Short-term impacts: Increased consumer spending, potential decline in student loan approvals.

- Mid-term impacts: Changes in educational funding models, shifts in public policy regarding student loans.

- Risks: Stricter lending practices, potential rise in tuition costs as institutions adapt.

- Opportunities: Growth in financial counseling services, innovation in alternative education funding solutions.

Regions with high concentrations of student debt, particularly urban areas with numerous colleges and universities, will likely experience significant economic shifts. As borrowers navigate the bankruptcy process, local businesses may benefit from increased spending, while educational institutions may need to adapt their financial models to remain competitive and accessible.

A: Not all student loans can be discharged in bankruptcy. Federal student loans typically require a higher standard of proof to show undue hardship, while some private loans may be easier to discharge. A: The process involves filing for bankruptcy and then filing an adversary proceeding to prove undue hardship. This can be complex and often requires legal assistance. A: Recent trends show an increase in the number of borrowers successfully discharging their student loans, reflecting changes in legal interpretations and borrower awareness. A: Discharging student loans can provide immediate financial relief, but it may also impact credit scores and future borrowing capabilities for the borrower. A: Yes, alternatives include income-driven repayment plans, loan forgiveness programs, and refinancing options which may provide relief without the need for bankruptcy.

Frequently asked questions about student loan bankruptcy

Looking ahead at the future of student loan bankruptcy options

The increasing number of student loan borrowers successfully discharging their debts through bankruptcy highlights a significant shift in the legal landscape. As courts become more receptive to these cases, it is essential to understand the broader implications for borrowers, lenders, and policymakers alike. This trend suggests a growing recognition of the financial burdens faced by graduates, prompting a reevaluation of the existing student loan system and its impact on individuals’ financial health.

As more borrowers navigate the complexities of bankruptcy, it is crucial to consider the potential changes in legislation and public perception surrounding student loans. Stakeholders should remain vigilant about evolving legal precedents that may influence future borrowing practices and the overall approach to student debt relief.

- Increased Awareness: Borrowers are becoming more informed about their rights and options, leading to higher rates of bankruptcy filings for student loans.

- Legal Precedents: Ongoing court cases may set important precedents that could further ease the path for future borrowers seeking debt relief.

- Policy Reforms: Lawmakers may be prompted to consider reforms in student loan policies, potentially leading to more favorable conditions for borrowers.

- Financial Literacy: There is a growing need for enhanced financial education to help borrowers make informed decisions about their loans and potential bankruptcy options.

- Market Impact: Lenders may need to adjust their risk assessments and lending practices in response to the changing landscape of student loan discharges.